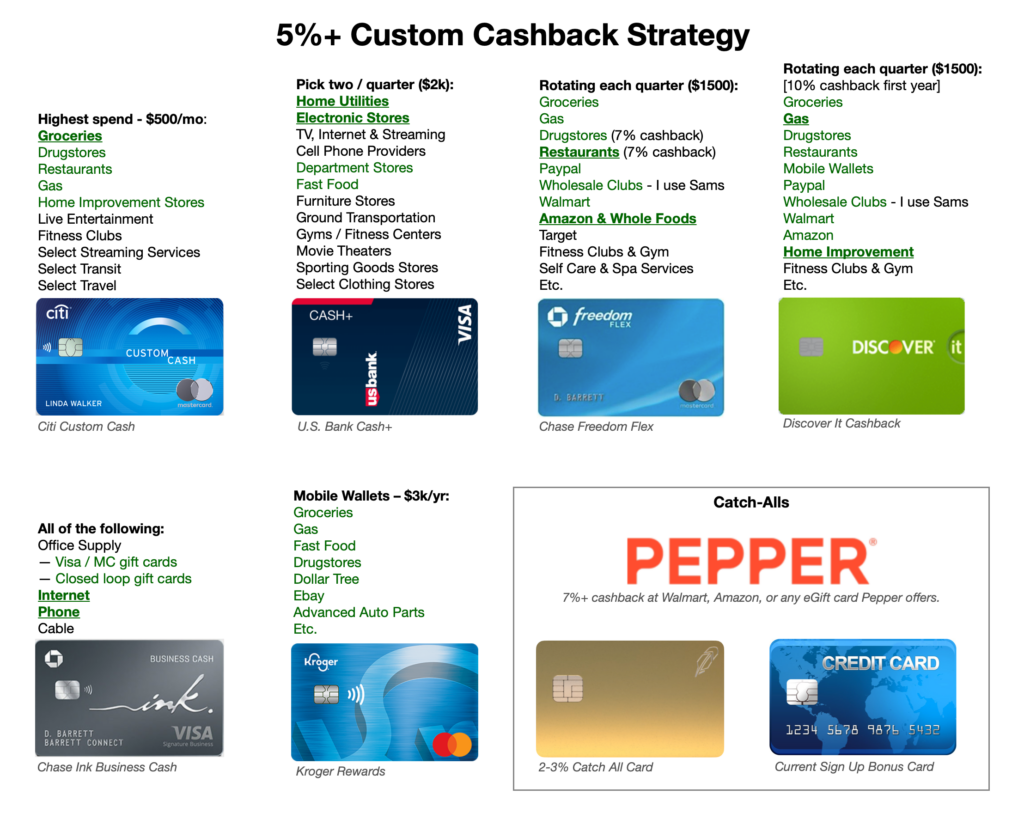

Well I just logged into the Chase portal and found out the Chase Freedom 2024 Q3 rotating categories will be Gas Stations & EV Charging, Select Live Entertainment & Movie Theaters. A couple weeks back we found out that the Discover It 2024 Q3 categories will be Grocery Stores & Walmart. So now knowing all this, it allowed me to formulate my 5%+ Custom Cashback Strategy for next quarter, which is as follows:

| Chase Freedom Flex | Gas Stations — won’t spend in entertainment & movies |

| Discover It | Groceries — using Pepper for Walmart 7%+ |

| Citi Custom Cash | Restaurants |

| Kroger Rewards | Mobile Wallet Purchases which include Drugstores |

| US Bank Cash+ | Utilities & Electronics Stores — Best Buy, Apple, etc. |

| Chase Ink Cash | Internet & Phone |

| Pepper App | For 7%+ back on Amazon, Walmart, Sam’s, Autozone etc. |

| Catchall / SUB | Chase Ink Premier (catchall) / Citi Strata Premier (SUB) |

All of the above cards are in my Apple Wallet. All my gas, grocery, drugstore, fast food purchases, etc. are done with Apple Pay using the appropriate card. The only two physical cards I’ll need to carry this coming quarter are my catchall as well as Citi Custom Cash for restaurant purchases — for those who don’t take Apple Pay.

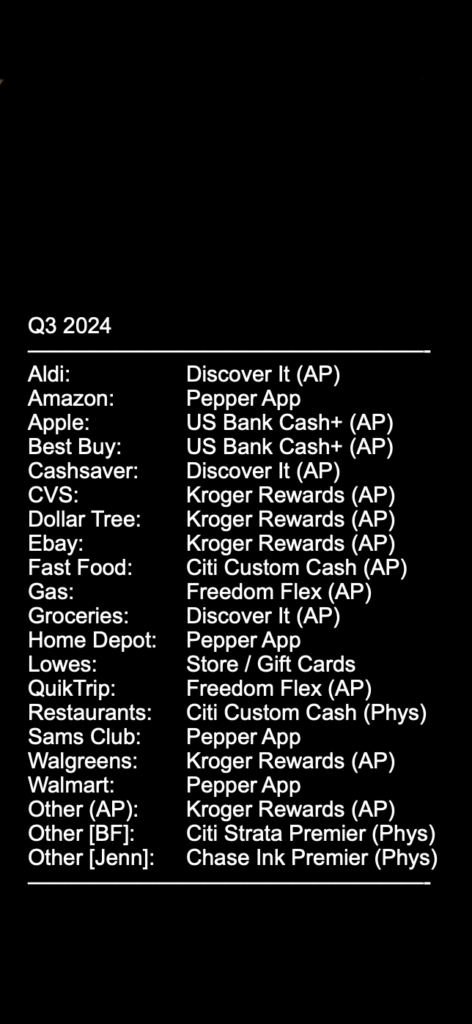

I use a unique iPhone lock screen wallpaper that I generate each quarter in the free Mac OS Pages application — takes about 5 minutes — which tells me which card to use for what, whether via Apple Pay (AP) or with the physical card (Phys). Here’s the iPhone wallpaper for this coming quarter.

So with the above say I am at Aldi and I don’t recall which card to use. I just pull my iPhone out of my pocket and the lock screen wallpaper automatically pops up. I look for Aldi and see I should pay with Discover It. So then I double click the button on the side of the phone to get into Apple Pay and then select my Discover It card, wave it over the e-reader, done! I have this lock screen wallpaper installed on both my phone as well as my boyfriend’s. I have all my cards listed above loaded into his Apple Wallet as well. With this setup he seems to never use the wrong card — getting 5%+ cashback like everywhere.

People say a customized cash / rotating category card setup like this is complicated but we have it made it very simple with this unique method we use. It takes 5 minutes to make the plan and 5 mins to create the wallpaper. Only 10-15 minutes each quarter for the setup. It’s all automatic and self explanatory. No physical card labeling is needed as this wallpaper covers both physical cards as well as cards loaded into Apple Wallet.

Note: of course if and when I am working on a credit card SUB and need the extra spend, I put the 5%+ cashback strategy on the back burner until I feel comfortable I have had enough spend on the SUB card. However, for me it makes me happy to know I can get 5%+ cashback at most places when not working on a SUB.

Here is a diagram I made of my current 5%+ Custom Cashback Strategy. The items which are underlined are the current categories for 2024 Q2.

I have backtested this setup with several years of rotating category data and this setup fully & easily covers all of my grocery, gas, dining and drugstore purchases every quarter — with the rare occasion of only 3-4% cashback dining inside a restaurant which is not of the fast food variety. With this setup I not only get these four essential categories covered, but additionally get any extra bonus categories a rotating category card might offer a particular quarter — e.g. say three months of 5% cashback on mobile wallets purchases using Discover It, up to $1500. I also really like that the Kroger Rewards card is a great gap filler to cover any of the four essential categories, but additionally covers any other purchases at merchants which take Apple Pay — e.g. eBay, dollar stores, auto parts stores, USPS, clothing & footwear stores, sporting goods stores, cinemas, etc.

For us this setup covers a lot of categories and is very easy for us to use — the iPhone lock screen wallpaper along with Apple Pay is what really makes this work for us, along with the Kroger card. Additionally as mentioned in the About page we are fairly frugal here and haven’t had any issues with the spend caps of each of these 5% cashback cards. We are very happy. I am sure this will evolve over time as we get more interesting cards.

Miscellaneous Tips. Have the due date on the Citi Custom Cash set to be such that the statement date will always be at very end of the month — this way the card is more in sync with all the other 5% cashback cards according to your overall quarterly plan. The due date on my Citi Custom Cash is set to the 23rd, which results in a statement date of the 28th, which works for all months including February.

Here’s a bonus hunter holding the six 5% cashback cards mentioned above in my current strategy — a.k.a. 5% Custom Cashback Hexafecta.

Honorable Mentions

Chase Amazon Prime. I do have this card but rarely use it as I am often not subscribed to Amazon Prime — so I only usually get 3% cashback there if I do use it. I am not fond of how much Amazon has recently increased the cost of prime membership — along with adding commercials to Prime Video — so I usually wait until I have $35+ in the cart before I purchase anything so I can get free shipping on it.

Occasionally I do subscribe to Amazon Prime if they offer it for $1.99 for one week or $7.99 for a month — or sometimes an entire month for free! I subscribe and immediately cancel so it doesn’t renew. When I do have a brief membership with them my Chase Amazon Prime card gets 5% cashback during that time period; additionally I’ll perhaps binge watch a particular TV series on Prime Video.

Pepper currently is a good substitute for Chase Amazon Prime as I can get 7%+ cashback with it, buying the exact size Amazon gift card I need for a particular purchase, not having to carry a gift card balance.

Citi Custom Cash — Additional Cards. I currently have a single Citi Custom Cash card. Due to my low monthly spend requirements along with my purchasing habits, I have backtested what would happen if I added an additional Citi Custom Cash: it wouldn’t get much use if any at all. Every quarter, depending on the rotating categories of the Chase Freedom and Discover It cards, the Citi Custom Cash card takes on a gap filling role, which is for Groceries if neither of the rotating category cards offer it for a particular quarter. Of the four essential categories — groceries, gas, drugstores & restaurants — by far the most use the Citi Custom Cash card would get is for “groceries”. Groceries run the two of us about $250 per month total. Our real grocery total each month is actually around $400 per month between the both of us, eating a low carb diet; however Citi doesn’t count grocery purchases at Walmart and Sam’s Club, where we spend about $150 per month total.

If interested, I have referral links for most all of the custom cash type cards mentioned above on my referrals page — Discover It, Freedom Flex, Kroger Rewards, Chase Ink Cash as well as the Pepper App. (Some of the referral links are mine and two others are from a couple friends.)

My good friend JD suggested the lock screen wallpaper idea a while back. It’s so much better than my original idea of using a clear iPhone case with a printed list on the back of the phone underneath.

The Kroger Rewards card is severely underrated. I’m surprised more people don’t talk about it. Great article!

Yeah, assuming one can cap the Kroger Rewards card with $3000 of spend, it gives the individual $90 more per year over using a 2% catch all card — $150 cashback versus $60. Ninety times, let’s say 30 years, is 90 x 30 = $2700 in extra cash. If one invested $90 per year into a security which gives an average 7% annual return, over thirty years, that $2700 invested would be around $8500 after those 30 years. https://cashbackcow.io/calculators.

Interesting related links:

Credit Card Setup That Maximizes 5% Cash Back as Much as Possible!

A member of RJ’s Discord channel said he is getting 5% cashback at eBay with Department Stores on US Bank Cash+. So I just changed one of my US Bank Cash+ categories to be Department Stores for next quarter instead of Electronic Stores — the other being Utilities of course. %5 Cashback at eBay versus Best Buy or Apple is more valuable to me. I can get 7%+ cashback at Best Buy with Pepper App anyways. I rarely buy anything from Apple as I usually find better discounts on their products elsewhere — e.g. Amazon where I get 7%+ cashback as well with Pepper. However, I tentatively have Apple purchases set to be covered with Kroger Rewards via Apple Pay if needed. I’ll report back here to let you know if it works next quarter.

UPDATE 6/21/2024: If this does work — if in fact Department Stores category covers all eBay purchases — I will most likely get an Elan Max Cash Preferred card to augment my US Bank Cash+ card. I’d probably have the two cards setup like this: 1) US Bank Cash+ as Utilities and Department Stores 2) Elan Max Cash Preferred as Department Stores and Electronic Stores. This would give me around a $3000 spend cap per quarter for eBay purchases assuming I didn’t buying anything under the Electronic Stores category — my utilities total around $1000 for three months. I am frugal as you know and like to buy used when I can, and often if one is patient enough they can find very good deals on items from eBay. Another option of course for eBay purchases is my Kroger Rewards card, as eBay takes Apple Pay if you check out on the iPhone.

Regarding Furniture Stores category on US Bank Cash+, I never buy new furniture. I buy brand new condition couches for $75 from Facebook Marketplace. Recliner for $75. Dining table for $25. $750 dining chairs for $50 (Emeco Navy). Whirlpool top loading washing machine for $150 — easy serviceable DIY for decades on the cheap. I bought a really nice vintage oak teacher’s desk for $125 in excellent condition etc. I buy foam from The Foam Factory to make my own queen size bed for $500 which has lasted me 15 years — in 5 years I’ll pay $500 again for another 20 years use. [I build the base for mattress with 5 slats across sleigh bed, with 4×4 posts under each slat; then a layer of MDF screwed down to the 5 slats for the 9″ of foam layers to rest on. There is no box spring and zero sagging. Foam layers include 2″ latex (top), 5″ high density (middle) foam as well as 2″ memory foam (bottom).]

My BF is BOSS. It’s Q3 2024 now and well yesterday he went to the grocery store and bought the groceries with the Discover card. He also stopped by the gas station mini market to get us some gum and he used the right card there as well, the Freedom Flex. Then today he went to Burger King to get something and he used the Citi Custom Cash. PERFECT! 5% cashback on all. He did all of this via Apple Pay consulting our lock screen wallpaper 🙂 It really works well!

Have you looked into using https://cardpointers.com/pro/ and having it auto-select the right card?

If I understand correctly, on iOS (but not Android) it has a way to auto-updating passes so that the right card is presented at each store.

Since you are using Apple Wallet already this might give you a quick win, especially for your P2.

(caveat: I have not used cardpointers (pro or otherwise)